New Construction Starts in July Hold Steady

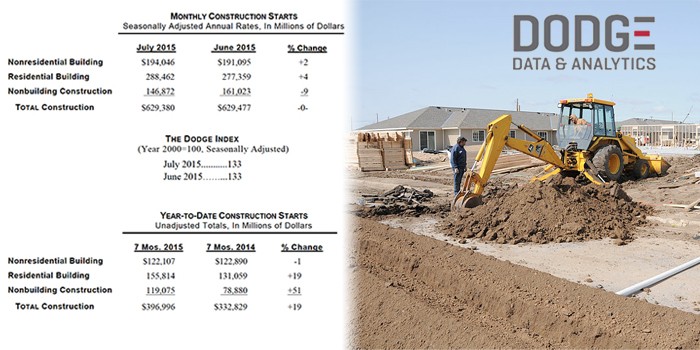

NEW YORK, NY – September 8, 2015 – At a seasonally adjusted annual rate of $629.4 billion, new construction starts in July were essentially unchanged from June’s pace, according to Dodge Data & Analytics. By major sector, nonresidential building showed slight improvement following its lackluster June performance, while residential building maintained the strengthening trend witnessed over the past several months. At the same time, nonbuilding construction in July continued to slide back from the exceptional activity witnessed earlier in the year that reflected the start of very large projects, including several massive liquefied natural gas terminals. Through the first seven months of 2015, total construction starts on an unadjusted basis were $397.0 billion, up 19% from the same period a year ago. Leaving out the volatile electric utility and gas plant category, total construction starts during the first seven months of 2015 would be up a more moderate 10% from the same period a year ago.

The latest month’s data kept the Dodge Index at 133 (2000=100), the same as June’s upwardly revised reading. While June and July were at the low end of what’s been reported so far in 2015, with the Dodge Index ranging from 133 to 156, they were still above the 125 average for 2014 as a whole. “The first half of 2015 showed wide swings in the pattern of total construction starts, affected by the presence or absence of unusually large projects,” stated Robert A. Murray, chief economist for Dodge Data & Analytics. “Amidst these top-line swings, the underlying trend of activity has been generally upward relative to last year. For nonresidential building, support has come primarily from its institutional segment, including educational facilities, transportation-related buildings, and amusement and recreational facilities. The commercial categories showed some deceleration during the early months of 2015, but positive real estate market fundamentals are expected to encourage renewed growth. Residential building has benefitted from this year’s heightened amount of multifamily starts, and even the single family side of the market is showing some hesitant signs of strengthening. The nonbuilding construction sector experienced robust activity during the opening months of 2015, for the most part related to the start of unusually large projects, and it now appears to be settling back to a more sustainable pace. The improved performance of the U.S. economy in the second quarter of 2015, with GDP rising 2.3% after a very weak first quarter, should help both nonresidential building and housing going forward. Nonbuilding construction will be helped in the near term by Congress recently passing a stopgap, three-month $8 billion surface transportation extension.”

Nonresidential building in July increased 2% to $194.0 billion (annual rate). The commercial categories as a whole bounced back 12% in July, after retreating by the same percentage amount in June. Office construction climbed 7% in July, reflecting groundbreaking for several noteworthy projects. These included the $232 million Bridgestone Americas office tower in Nashville TN, the $150 million Seaport Tower in Boston MA, a $100 million data center in Lowell MA, and a $100 million portion of the Toyota Corporate Campus in Plano TX. “During the first half of 2015, office construction appeared to level off after its substantial 35% gain in 2014,” noted Murray. “On the positive side, office vacancy rates continued to recede through this year’s second quarter, the volume of office construction is still quite low by historical standards, and the July pickup in construction starts may well be an indication of renewed growth to come.” Store construction in July improved 6%, helped by the start of the $40 million Wade Park Shopping Center in Frisco TX. Warehouse construction in July rebounded 28% after a weak June, and included groundbreaking for a $48 million Home Goods distribution center in Tucson AZ. Hotel construction, which has been the one commercial property type to register healthy year-to-date percentage growth, slipped 4% in July. The latest month still included the start of several large hotel projects, such as the $79 million phase 2 of the Kalahari Resort and Water Park in Pocono Manor PA, the $76 million renovation to the Atlanta Marriott Marquis Hotel in Atlanta GA, and the $75 million hotel portion of the $175 million Hilton Statler Hotel and Residences in Dallas TX. New manufacturing plant construction starts were generally subdued in July, falling 39% from June, and substantially lower than the elevated amounts back in February and April that featured the start of several huge petrochemical plants.

The institutional building group in July eased back 1%, receding for the second month in a row after improved activity earlier in 2015. The educational facilities category dropped 20% after strengthening during the previous three months. Even with the decline, July included the start of such projects as a $162 million research and development building in Cambridge MA and a $112 million elementary and middle school campus in Seattle WA. Healthcare facilities in July fell 15%, maintaining the up-and-down pattern that’s been present in 2015, even with the July start of a $250 million hospital tower in Provo UT. The smaller institutional categories all registered gains in July. Transportation-related buildings jumped 120%, helped by the start of a $200 million rail service facility in Croton On Hudson NY. The amusement and recreational building category climbed 49%, helped by the start of a $130 million student center at the University of Kentucky in Lexington KY and a $123 million music hall renovation in Cincinnati OH. Both the public buildings category and churches rebounded from very weak activity in June, posting respective gains of 58% and 32%. The public buildings category was supported by the July start of a $275 million detention center in Indio CA.

RELATED Single-Family Gains Push Housing Starts to Highest Level Since 2007 , Housing Markets Continue to Show Gradual Improvement , Dodge Momentum Index Rebounds in July, Roofing Demand and Construction of New Housing Units to Surge by 2019, Reports Say , Multifamily Surge Pushes Housing Starts Up 9.8 Percent in June , Sprayfoam 2016 Convention & Expo to be Held in Orlando

Residential building, at $288.5 billion (annual rate), advanced 4% in July. In similarity to recent months, the main residential push in July came from multifamily housing which surged 21%. July included the start of 16 multifamily projects valued each at $100 million or more, led by the following – a $468 million apartment building in Long Island City NY, a $445 million condominium building in New York NY, and a $358 million multifamily building in Miami FL. At the seven-month point of 2015, the top 5 metropolitan markets ranked by the dollar volume of multifamily starts, with the year-to-date percent change, were as follows – New York NY, up 79%; Miami FL, up 65%; Washington DC, up 6%; Los Angeles CA, down 11%; and Boston MA, up 92%. Single family housing in July slipped back 4%, continuing its up-and-down pattern around a modestly rising trend. The year-to-date dollar amount of single family starts at the U.S. level was up 14%, due to this pattern by major region – the West, up 22%; the South Atlantic, up 19%; the South Central, up 10%; the Midwest, up 6%; and the Northeast, down 3%.

Nonbuilding construction in July dropped 9% to $146.9 billion (annual rate). The decline came as the result of diminished activity for most of the public works categories, which fell 13% as a group. Highway and bridge construction retreated 19% in July, making it three out of the past four months that weaker activity has been reported, which follows the surprisingly strong pace in early 2015. “The uncertainty arising from the expiring extension of the surface transportation legislation on July 31, along with the depleted Highway Trust Fund, likely played some role in July’s pullback for highway and bridge construction,” Murray stated. Despite the decline, there were several large highway and bridge projects entered as July construction starts, including the $429 million Southern Ohio Veterans Memorial Highway in Portsmouth OH, the $264 million Belt Shore Parkway Mill Basin Bridge replacement in Brooklyn NY, and the $187 million Interstate 85 widening and reconstruction in North Carolina. The environmental public works categories in July all reported a diminished volume of construction starts, as follows – river/harbor development, down 20%; water supply construction, down 23%; and sewer construction, down 27%. The “miscellaneous public works” category (which includes such diverse project types as site work, pipelines, and mass transit), ran counter in July with a 29% gain. Large miscellaneous public works projects that reached the construction start stage in July included the $700 million expansion of the Creole Trail natural gas pipeline in Louisiana, a $495 million oil pipeline replacement in Illinois and Indiana, and a $195 million Northeast Rail Corridor project in Connecticut. The electric utility and gas plant category in July increased 9%, due to the start of several large power plant projects – an $850 million natural gas-fired power plant in Maryland, a $420 million wind farm in Maine, a $337 million wind farm in Texas, and a $191 million solar power facility in Colorado.

The 19% advance for total construction starts on an unadjusted basis during the first seven months of 2015 was due to double-digit gains for residential building and nonbuilding construction, while nonresidential building slipped slightly. Residential building year-to-date was up 19%, as a 34% jump by multifamily housing joined the 14% rise by single family housing. Nonbuilding construction year-to-date soared 51%, with electric utilities and gas plants up 268% while public works registered a 12% gain. As 2015 is progressing, the huge year-to-date increase for nonbuilding construction is becoming smaller. Nonresidential building year-to-date receded 1%, reflecting the downward pull from a 22% decline for the manufacturing building category, while institutional building was up 6% and commercial building was up 1%. By geography, total construction starts during the January-July period of 2015 performed as follows – the South Central, up 39%; the Northeast, up 29%; the South Atlantic, up 17%; the West, up 6%; and the Midwest, up 4%.

About Dodge Data & Analytics: Dodge Data & Analytics is the leading provider of data, analytics, news and intelligence serving the North American construction industry. The company’s information enables building product manufacturers, general contractors and subcontractors, architects and engineers to size markets, prioritize prospects, target and build relationships, strengthen market positions, and optimize sales strategies. The company’s brands include Dodge, Dodge MarketShare™, Dodge BuildShare®, Dodge SpecShare®, and Sweets. To learn more, visit www.construction.com.